APChanel // Shutterstock

Freight carriers pivot to weekly rate updates amid global fuel volatility

The beginning of April 2026 saw the U.S. extend its national security tariff umbrella to the healthcare sector, imposing a massive 100% duty on foreign pharmaceuticals to decouple medical supply chains, Freight Right reports.

This aggressive unilateralism stands in stark opposition to the EU’s recent diplomatic successes, such as the inevitable ratification of the Mercosur deal, which seeks to secure critical minerals through cooperation rather than coercion.

Meanwhile, the World Trade Organization’s latest figures highlight a shifting global guard, with the UAE’s rise to a top-10 exporter occurring just as the organization slashes global growth forecasts to 1.9% amidst a surging energy crisis.

Collectively, these events suggest that while the U.S. is doubling down on protectionist fortress economics, other major powers are aggressively forming new, non-U.S.-aligned trade corridors to mitigate the inflationary impact of $110 oil and high Western tariffs.

This Week’s Ocean, Air and Freight Markets

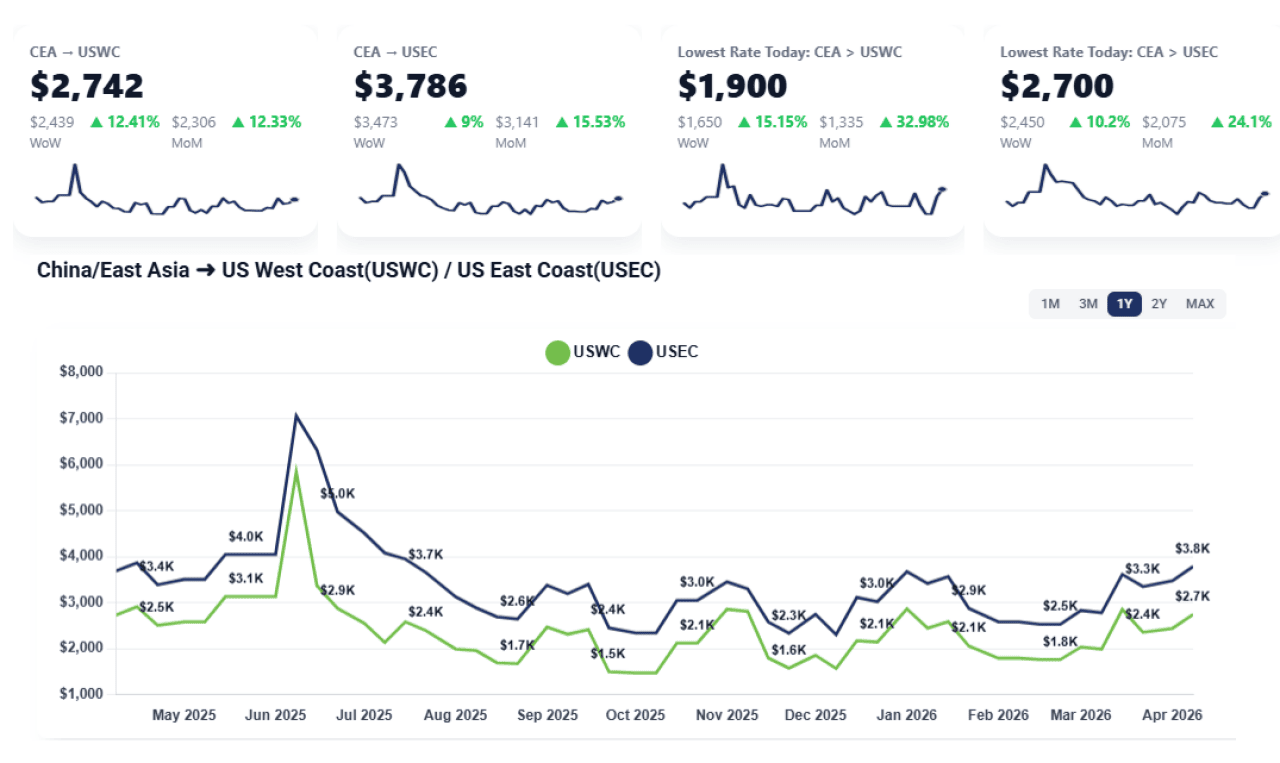

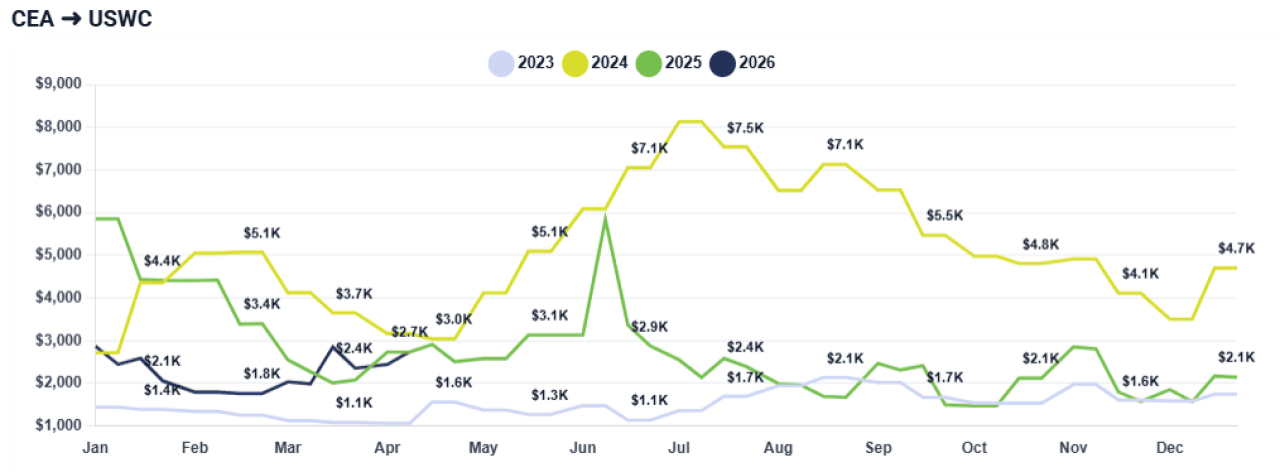

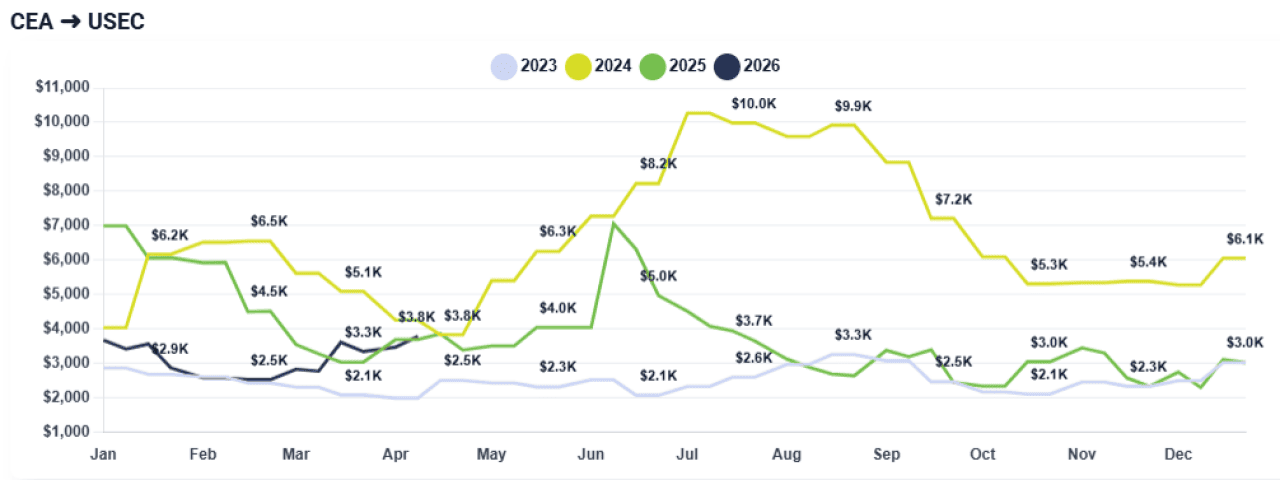

China-U.S. Ocean Freight Market:

Ocean freight rates from China to the U.S. remain highly volatile week-over-week, with this week’s increases driven primarily by fuel surcharges rather than base rate adjustments.

CEA to USWC: Rates are holding relatively steady at the base level, but all-in pricing has increased to approximately $2,700 per FEU, up from roughly $2,400–$2,500 last week due to a newly introduced ~$300 fuel surcharge per container.

CEA to USEC: Similarly, USEC pricing is experiencing incremental increases driven by fuel costs, with all-in rates trending upward in line with USWC dynamics.

Notably, carriers have shifted from bi-weekly rate releases to weekly updates, reflecting a highly volatile environment. While base ocean freight rates have remained relatively constant, the overall cost to shippers has increased due to the implementation of significant surcharges.

Freight Right

Freight Right

Freight Right

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

What Happened This Past Week

Carrier Profitability Strategies: Airlines and ocean carriers are aggressively managing space to maximize profits. This includes the continued use of blank sailings to ensure services remain sustainable and profitable.

Stagnant Volume: Despite the increase in costs, actual freight volume remains slow with no significant spikes in demand observed.

Air Freight Spillover: Air freight rates remain high at $8–$9 per kilo, with severe space constraints as airlines hold back capacity for the highest bidders, adding pressure to overall logistics budgets.

Looking Ahead:

The outlook for the remainder of April remains unstable. The industry is moving away from predictable bi-weekly rate extensions; it is anticipated that the second half of the month will continue to be broken into smaller, weekly pricing portions.

As long as fuel price volatility persists, shippers should not expect a simplification of the rate structure. The market is currently in a “wait and see” posture, with no signs of the current upward pressure slowing down for at least the next week. Importers should prepare for continued “headwinds” where pricing remains high despite sluggish volume.

This story was produced by Freight Right and reviewed and distributed by Stacker.

![]()